One often overlooked but critical process of the oil and gas industry is water management. The Shale Revolution was primarily possible thanks to the development of two separate techniques. Hydraulic fracturing (aka. fracking) and Horizontal Drilling.

Hydraulic fracturing injects water, sand and chemicals to create small fractures in rock formations to release oil and gas from where it is trapped. Once the oil and gas is captured back into the surface, the amount of water (also known as produced water) that’s recovered equals 4:1 ratio to oil (figures from West Texas basins). So for 1 barrel of oil, you get 4 barrels of produced water.

So what do companies do with this produced water? They have two options: 1) Inject it back into permitted underground wells, 2) Treat it for industrial/ agricultural use or recycle it back specifically for oil and gas operations. Both of these options require large operations that include:

- Using pipelines to transport the produced water

- The right of way of the land you are using to move the water

- The water handling facilities

- The water recycling facilities

So who handles all the produced water from oil and gas operations?

Upstream oil and gas companies are responsible for managing the water produced from their wells. Initially, these companies had their own operations in house. This was a small headache for them when the volume of water produced was low and could often be moved by truck, but as these companies started to drill deeper, the content of water to oil started to grow (specifically in West Texas).

Additionally, companies started to face another challenge due to new regulations that were put in place to minimize the environmental impact. So once a by-product operation, companies started to require a full fledged infrastructure and specialized teams that large upstream oil and gas companies saw as a burden.

Over the past years, a large number of companies have emerged that specialize only in water handling in the Permian Basin (some of them include WaterBridge Resources, Select Water Solutions, Oilfield Water Logistics, Aris Water Solutions or Solaris Water Midstream).

So how do these companies make money?

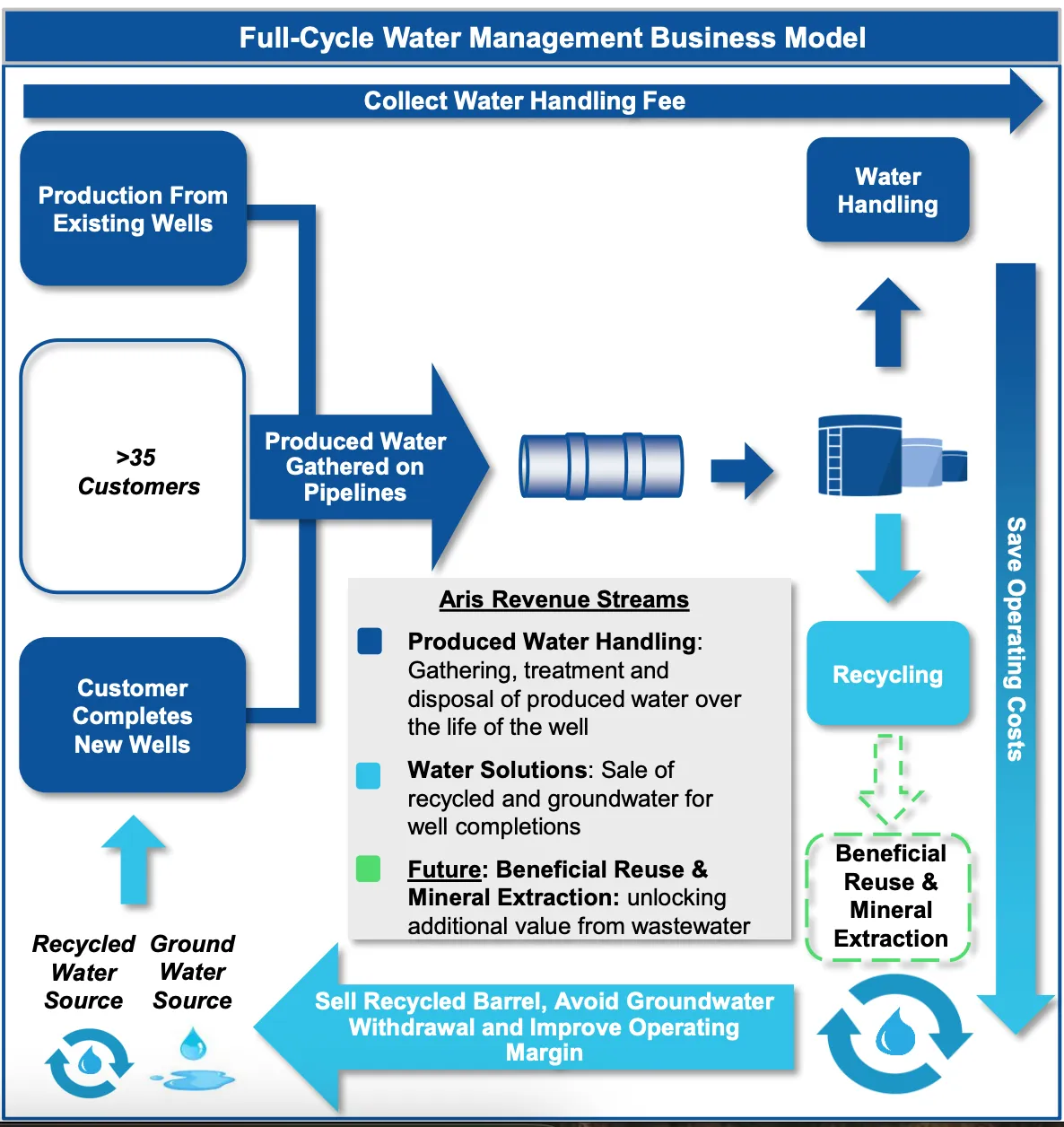

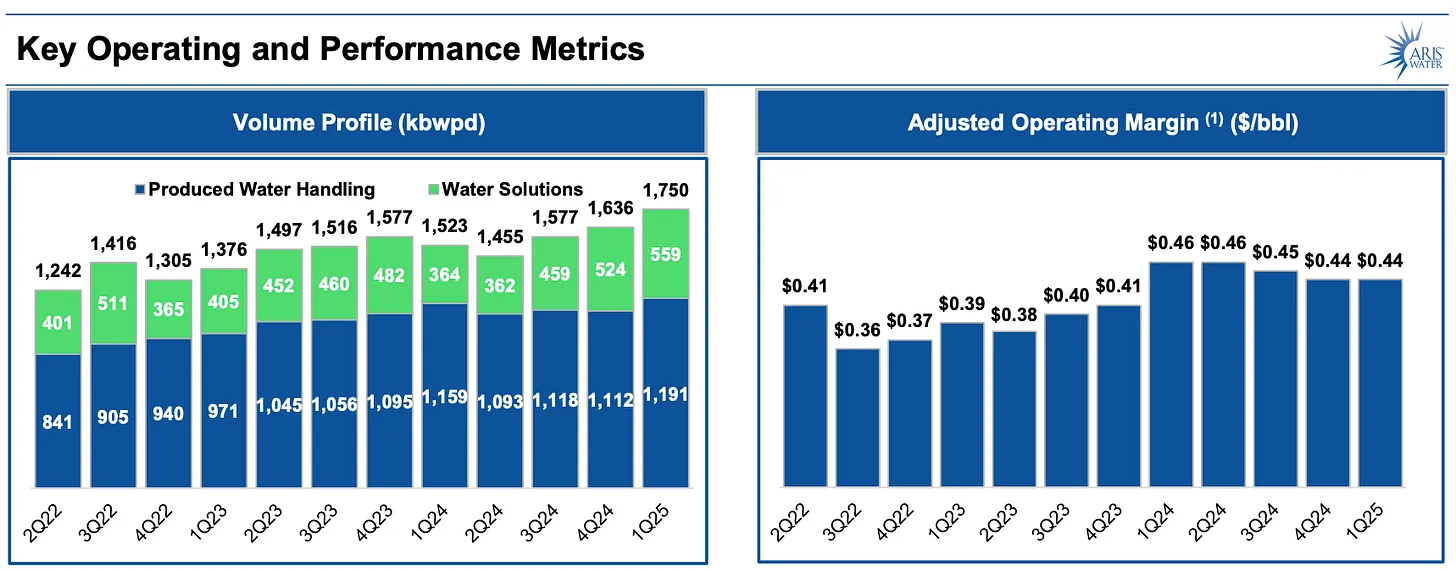

Their main source of revenue is tied to the volume of produced water they move from existing or new oil and gas wells. This volume is measured as ‘kbwpd’ or thousand barrels of water per day. Rough numbers indicate that for every barrel of oil that’s extracted, upstream companies pay $0.85-$1 to water companies for managing the produced water.

Additionally, water companies also sell the recycled water which in some cases can make up to 30% of their share of revenues (vs. 70% produced water). Below is a good representation on how the business model works (from Aris Water Solutions):

After the pipeline transportation and handling is done, the operating margin these companies can achieve is as high as $0.40-$0.45 per barrel of oil (or over 50% in some cases).

There are several factors that influence these margins and may vary company to company:

- Pipeline infrastructure: built-out water pipelines (vs. trucks) have higher margins due to lower opex.

- Land ownership: do they operate within their own land or do they have to pay land owners to transport water through their property.

- Scale: larger companies can commit to a certain minimum volume that allows them to close better pricing power and long-term contracts.

- Recycling: how much of the produced water is sold back to either oil and gas companies or other industries.

So what’s the competitive advantage of these companies?

In order to commit to certain volumes with upstream companies, water management companies need a reliable and large pipeline infrastructure. This is what takes the majority of their capex allocation and it fluctuates significantly based on new projects.

In my opinion, management’s discipline to balance their capex growth with their operating cash flow (OCF) is what can make or break these companies. Aris is a clean self-funding story where their OCF ≈ 1.5-2× capex. This allows them to return capital to shareholders with a growing dividend.

Other companies, such as Select Water Solutions, are sacrificing near-term free cash flow for a larger footprint. If depressed oil prices remain, this strategy may be questioned by the market and a lower multiple may be granted. Note that today, both companies have a similar trailing P/E of 26 but their forward P/E differ significantly (with Aris at 15x and Select at 20x).

Another aspect to consider, although less important than the above, is the ability of these companies to find further uses for their recycled water. Today, the majority of that is sold back to companies such as Chevron, ConocoPhillips, etc., which makes their business very tied to the oil and gas industry.

Diversifying outside the O&G industry is something I’m looking forward to seeing these companies achieve. Some market participants are optimistic that if there is a large scale development of data centers in the Permian, some of this water can be used for data center refrigeration. I like this optionality but I would not assign any value to it until we see the hyperscalers committing capital to develop data centers in the Permian.

So why own Aris Water Solutions?

First, I believe oil consumption is not going anywhere in the next 20-30 years. Thus, the need to handle produced water is also not going anywhere. While oil prices can remain depressed for a long time for a diverse set of reasons, the market will finally bend and price will shoot to the upside.

Second, I believe we are in a structural inflationary period that will take some time to correct. During the past 20-30 years the world has experienced the largest disinflationary period in modern history and it has already come to an end. We no longer have:

- the largest demographic cohort (Baby Boomers) pouring capital into markets, thus lowering capital costs for corporations

- China’s ‘unlimited’ population growth pouring cheap labor into the mix

- the USA acting as the main node of a globalized world by providing secured maritime trading routes with almost every country

- Russia opening its cheap commodities markets in the 90s after the collapse of the Soviet Union

- balanced/semi-balanced deficits across the world that allow for a moderate issuance of treasuries that can be bought by ‘real’ parties (i.e. not central banks)

Third, in the type of environment I outlined above (structurally inflationary), I prefer to own real assets that are capital light businesses (a term I first learned from Murray Stahl from Horizon Kinetics). While Aris owns real assets in a prime location (pipeline infrastructure across the Permian) they do need capex to expand and fuel their growth. As mentioned above, Aris management has made it very clear that they will balance their capex according to market conditions, making decisions with their shareholders in mind.

And finally, the company’s business growth drivers are simple and easy to bet on:

- We are going to see higher oil to water ratios as O&G producers drill deeper in the basin. Remember, water companies charge by volume of the produced water they handle.

- Aris’s recycled water technology will keep improving over time, increasing the amount of water they can sell back. This will help expand the operating margin per barrel of oil without larger capex increases.

What are some of the key risks of owning Aris?

First, they don’t own the land where they operate. They need to constantly close contracts with companies such as LandBridge or Texas Pacific Land to use their surface for their operations. They recently purchased the McNeill Ranch for $45M to try and optimize for this factor.

Second, 75% of their business is concentrated within 4 customers (ConocoPhillips accounts for 38%). Although they have long term contracts with them and they are very large O&G companies, they are heavily reliant on these producers’ successful operations.

Finally, I don’t see it as a risk but something I don’t like is that insiders own less than 10% of the company and they haven’t bought any shares recently. The company IPO’d in 2021 and saw its normal selling of private investors. While I believe the sell pressure from the IPO is over, I’d like to see insider ownership increase.

So is the current valuation of Aris Water Solutions attractive today?

Today you can buy Aris for 26x trailing P/E, which would give us an earnings yield of 4%. Let’s be honest, not great at all. The Oil & Gas Midstream industry overall is trading at a weighted average P/E of ~18.0×. However, the company has been growing its recycled water business at 54% y/y (Q1'25 figures) and expanding its operating margin consistently. Thus, if we use the forward looking P/E of 15x, then we get an earnings yield of 6.6% which starts to get more attractive.

I believe the company is trading at a premium due to its growth projections as well as its focus on returning capital to shareholders. If we don’t see a large decrease in O&G operations over the coming months and oil prices find their support at $65, this premium can be justified.

I have built 50% of my position at an average price of $23. I am in no rush to buy my remaining position. For a $1.2B company, I expect lots of volatility which I’ll be happy to be a buyer of if it surprises to the downside.