Three months have passed since Ethereum switched to proof of stake. Despite the initial worries and doubts from many, the blockchain has been running without a hitch.

The main worry that followed us before and after the merge is still here. The issue that three entities control more than 50% of the network remains unsolved. Do we need to address this? Absolutely! Is there cause for alarm? Not as much as one might think. On the other hand, should we be worried that conventional financial systems are becoming more and more centralized? Absolutely; allow me to explain why.

Censorship resistance in its nature

The potential problem of Coinbase, Lido and Kraken jointly controlling over 50% of the chain is that they can choose which type of transactions they want to censor. All three of these entities have ties to US authorities, meaning that they could be asked to carry certain orders and censor specific transactions if needed.

The key reason why many support the concept of decentralized cryptoeconomics is its censorship resistance capabilities. This implies that no one can prevent you from making transactions or interacting with another party. It also means that nobody can exclude you from the chain due to certain activities. To make sure this censorship-resistance is enforced, Ethereum has a slashing mechanism in place to punish validators that refuse to validate blocks. The main objectives of this system are twofold — it makes attacking the network too costly, and it ensures validators act responsibly.

Essentially, this is how the process works:

- If less than 33% of the network refuses to attest to blocks, validators get their ETH reduced on a node to a point where the node is removed from the network.

- If more than 33% of the network refuses to attest to blocks, the penalty is rapidly applied to fall below the minimum threshold to run a node and the validator is booted from the network.

I believe that Ethereum’s strength lies in its transparency and the neutrality of its underlying mechanisms. Although network monopolies are bound to form, the influence that they are able to have is limited due to the clear and effective rules that the Ethereum chain enforces.

Traditional markets face a similar issue, however, I would argue that the rules and regulations in place are much less effective than what smart contracts can achieve.

TradFi’s weak governance

Monopolies are usually considered to be bad for the economy as they tend to lead to an increase in prices. The current method of controlling this is through anti-trust laws, which seek to regulate the activities of a firm to promote competition and stop unjustified monopolies. I wonder if these laws have really been successful or if a line of code in Solidity would be more efficient?

Over the past couple of decades, the amount of assets held in index funds has skyrocketed. People have realized that it is almost impossible to outperform the markets regularly. The most cost-effective way to have exposure to the markets and diversify your portfolio is through low-cost index funds (also known as passive funds). These funds are designed to replicate a specific index (e.g. S&P 500 or the NASDAQ). The consequence of this rapid rise in index fund ownership is that institutional investors, who manage these funds, have become the largest shareholders and controllers (i.e. voting power) of major corporations.

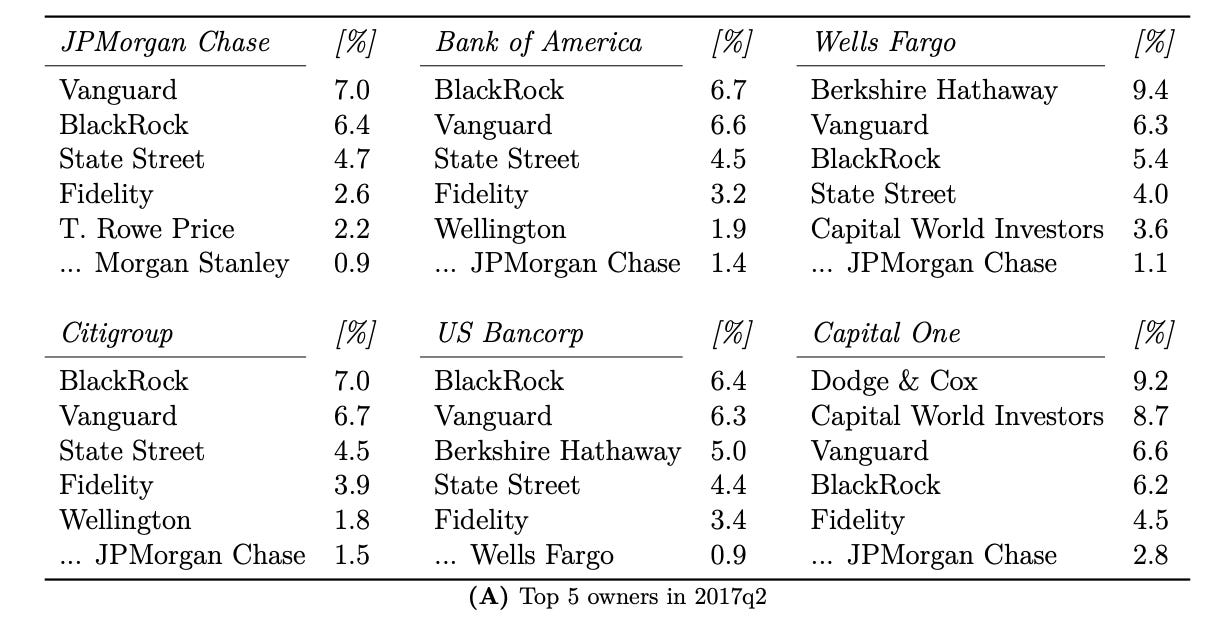

Similar to our concentration in Ethereum, in our traditional systems we have four big players: BlackRock, Vanguard, State Street and Fidelity. Combined, three of these institutions (BlackRock, Vanguard and State Street) are the largest individual stakeholders of 40% of the public companies operating in the United States and nearly 90% of the public companies listed on the S&P 500.

Moreover, the same investors mentioned earlier are also involved in actively-managed funds. In these types of funds, they make their own stock picks and have the power to sell stocks if businesses they are invested in do not comply with their suggestions. It is easy to see how much power they have over the companies they own, which is open to potential misuse. As an example, below is a look at the US banking industry which shows how centralized its ownership is (this is an issue that goes beyond the US and affects other major industries worldwide).

There are several papers that point out that such power and influence from institutional investors has been reflected in a diminished level of competition, an upward trend in prices, and a decrease in investments (combined with an increase in stock buybacks). As you can imagine, the same investors own the same companies and competing in prices is the ultimate thing they want to see since it will lower their profits.

Moreover, not complying with institutional investors’ advice can also impact executive compensation since they are the ones entitled to add/remove board members.

Conclusions

At first glance, comparing the centralized structure of Ethereum to the stockholders structure found in traditional markets may seem like a stretch, but I believe there are more similarities than differences. Being aware of these distinctions, and seeing how wide the gray area is in conventional markets, instills me with hope for a blockchain-based future. The governance of Ethereum isn’t flawless, but it’s a great improvement. The comparison in this article brings me to my three last takeaways:

Legislation is slow to be updated. This results in inefficiencies being formed by participants in the market. Passive investment has been on the rise for the last three decades and no serious modifications have been made to consumer protection via anti-trust regulations. On the other hand, Ethereum is constantly changing and suggesting new developments to create a flourishing ecosystem.

When laws are subject to interpretation, they can be difficult to enforce. Anti-trust laws have arguably been a key reason why big tech has been able to grow during the last decade (the fact that big tech’s products are mostly free has made anti-trust law inefficient, since the law mainly focuses on price competitiveness). Ethereum’s code, however, does not allow for interpretation — if certain transactions are being censored, the code immediately penalizes this behavior.

On-chain activity allows for better accountability and traceability. A lot of the decisions that happen in traditional markets aren’t clearly reflected in the company’s financial reports. This creates a loophole through which certain people with power can exert control over important decisions — for instance, the BlackRock CEO calling the Wells Fargo CEO to advise him against offering a particular type of loan, as it could jeopardize the profitability of other banks, is a clear example of what can’t be traced in the system.

Part of my argument on institutional investments’ impact in TradFi has been borrowed from the book Radical Markets by Eric A. Posner & Glen Weyl. If you are interested in radical and applicable policies to empower markets and improve our economy, I highly recommend it.